Liquid China Crashes As Traders Head For Exits

Simple Bear Necessities

The Hang Seng Index (or “liquid China”) crashed over none percent as the Shanghai, Capital Controls, I mean, composite rose 4.55% Alibaba is down over 8% with JD.com down over 10% in U.S. premarket.

All the “goodies,” such as copper, to fade are falling through a trap door.

I went over this in “Has Liquidity Turned To Support The Chinese Narrative?” It was important to manage your expectations - and trades - via the TMS Trading Ranges.

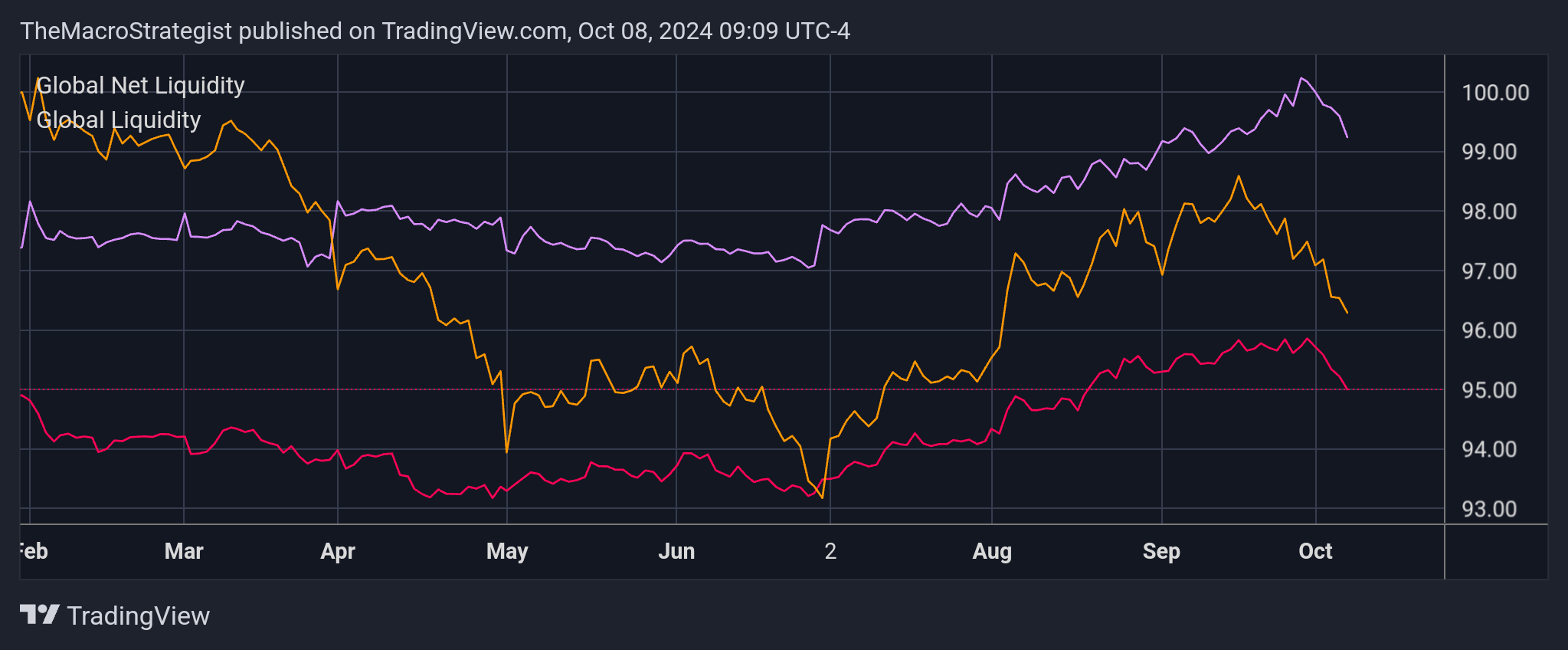

Both global liquidity (money supply proxy) and the US liquidity proxy are turning lower. This week's volatility in U.S. markets could be attributed to the lonshoreman strike, but, as this AM's trading ranges shown, US equities are moving from strong bulltrend to weak bull; and the VIX is solidifying into a strong bull trend.

The chart above has a huge difference in global liquidity than the same chart posted in the note linked above.

If we break it down, we see notable declines in western denominated (pink) liquidity as well as eastern denominated (purple) liquidity.

Remain more risk adverse, but if the relative strength trade in China is reversing, we could see inflows back into IWM, QQQ and SPY. If liquidity measures remain on the downside, US Bonds will remain pressured.