The Uemployment Picture

Irrationally Rational

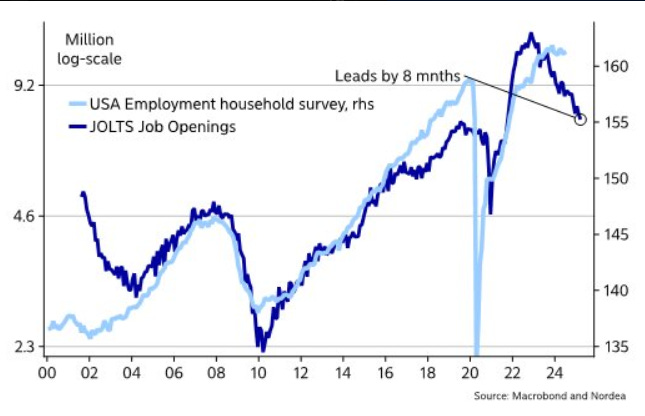

Employment Trends and JOLTS Data Signal Cooling U.S. Labor Market

The latest data on U.S. job openings and employment points to a cooling labor market, adding to the growing concerns about potential economic deceleration. As seen in the charts, the JOLTS (Job Openings and Labor Turnover Survey) Job Openings data is starting to lead a significant decline in both general employment levels and employment within specific sectors like construction.

General Employment vs. JOLTS Job Openings:

This chart compares U.S. employment from the household survey (light blue line) with JOLTS Job Openings (dark blue line). A crucial observation is that job openings (JOLTS) have historically led employment by about 8 months.

Over the last two years, job openings surged to historic highs, driven by pandemic recovery efforts, supply chain disruptions, and shifts in labor dynamics. However, we are now witnessing a sharp decline in job openings, which could signal an impending slowdown in employment levels.

The drop in job openings is significant because it suggests that the tight labor market of 2022 is easing, potentially leading to weaker hiring momentum in 2024. If this trend continues, it could lead to rising unemployment, especially as the decline in job openings has historically preceded broader declines in employment by several months.

Construction Sector Employment vs. JOLTS Construction Job Openings:

Focusing on the construction sector, the pattern is similar. Employment in construction (light blue line) has risen steadily since 2012, closely tracking the post-financial crisis recovery and the booming housing market, while construction-related job openings (dark blue line) have also followed this upward trend.

Notably, the JOLTS data for construction has started to fall sharply, leading employment by about 9 months. This sharp drop in job openings is a potential red flag for the construction sector, which has been one of the most sensitive industries to interest rate hikes. With borrowing costs for housing increasing due to the Federal Reserve's monetary tightening, demand for new construction is likely to decline further.

The chart also reflects a historical trend: during past economic cycles, whenever job openings in construction have dropped significantly, broader employment in the sector follows within months. This could indicate more pronounced layoffs or a hiring freeze within the sector, which could negatively affect GDP growth and housing-related industries.