The Macro Brief: Shanghai Scapegoat Covering China's Distress

The Macro Brief: Shanghai Scapegoat Covering China's Distress

Where Macro Meet Market

The International Monetary Fund (IMF) has finally revised lower its forecasts for global growth to 3.6 percent from 6.1 percent forecasted last year and the 4.4 percent in their forecast in January.

But none of this was unexpected, as I was forecasting decelerating growth in the U.S. and emerging markets, especially China:

“U.S. growth will continue to decelerate while supply-chain caused inflation could linger throughout the quarter.” - So Long 2021! What’s Poppin’ In Q1-22.

I even went ahead an expressed the viewpoint by being short emerging market debt ($EMLC) and equity ($EUM - heavy exposure to China).

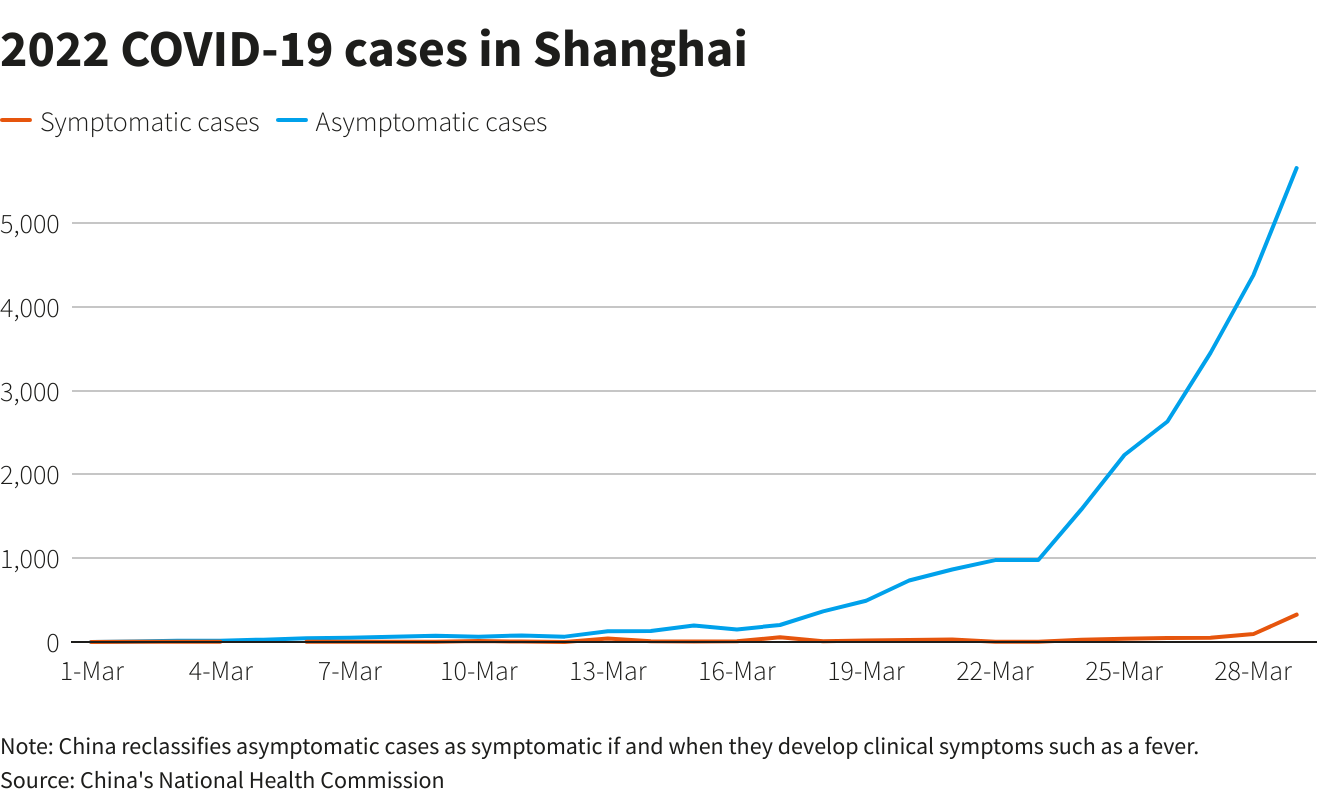

The idea that the Shanghai lockdown is legitimate is asinine.

If we look at import data, on its face it makes sense given the lockdowns. However, asymmetric cases didn’t start moving higher til the tail end of March.

Cases then exploded throughout April. But, is this rather a scapegoat for China growth deceleration?

There’s a theory that these lockdowns are being done to “put the hurt” on the U.S. and the West by fucking up supply chains further thus exacerbating consumer prices.

Think this out: then why is domestic demand falling off a cliff, particularly in March when case count was still rather mild?

Oil imports fell 14% YoY with Q1-22 imports down 8% YoY. Refined oil products are down a whopping 40% YoY. Natural gas imports are the lowest since October 2020. Copper imports were down 8.8% in March, too.

Is it any wonder why commodity prices sharply inflected lower in early March (before the spike in covid cases) when the largest consumer of commodities, globally, is out of the market?

Sign up for The Macro Strategist Pro annual subscription for 50% OFF. Only Available until next Monday!

Keep reading with a 7-day free trial

Subscribe to The Macro Brief to keep reading this post and get 7 days of free access to the full post archives.