The Macro Brief: Are Cross-FX Swaps Signaling Continued Dollar Strength? - Deer Point Macro

The Macro Brief: Are Cross-FX Swaps Signaling Continued Dollar Strength? - Deer Point Macro

Where Macro Meet Markets

This is an exclusive piece by Deer Point Macro for The Macro Strategist community. We strive to offer differing opinions and expert insight from thought provoking individuals.

Deer Point Macro will discuss how cross-currency swaps relate to U.S. dollar strength or weakness. Enjoy!

We’re currently offering 25% annual subscription to The Macro Strategist Pro where subscribers get exclusive charts, analysis and much more!

Something that has seemed to confuse many people especially those who have been more outspokenly bearish on the dollar is its strength in the face of all the geopolitical and macroeconomic events that seem to be happening simultaneously.

I will be discussing cross currency basis swaps (CCBS), and its relation to perceived dollar shortages and credit risk. This is a good indicator that can be used to help gauge the strength of the dollar, and the risk that the world is facing because of this dollar shortage.

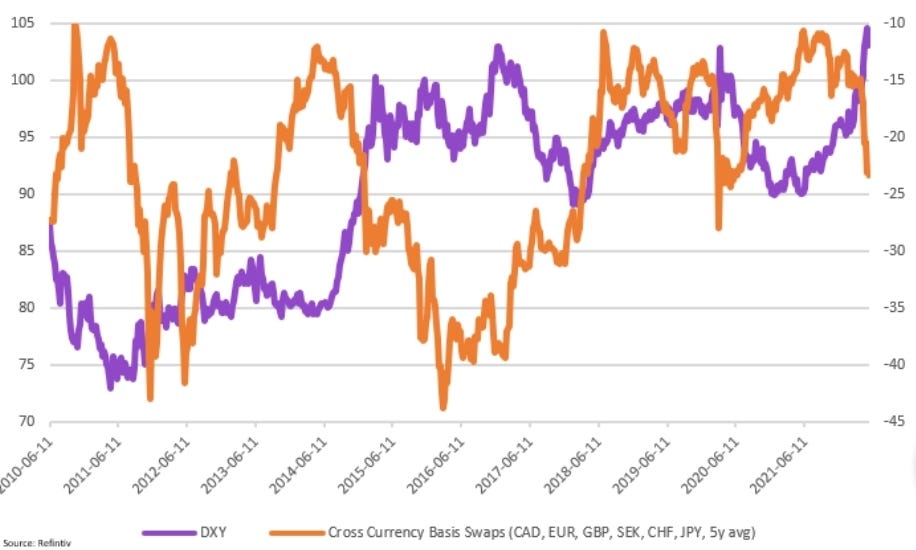

The first thing that needs to be discussed is the shortage of dollars we are seeing, and how it effects equity markets. There is a correlation and while the chart below is kind of busy hopefully this can help shed light.

What the Chart 1 is showing is that in times when USD funding is tighter or perceived to be tighter it comes on the back of global equity selling. This is to sell liquid assets and hopefully get into dollars.

If you look at Chart 1 what you will notice is many of the cross-currency basis swaps are heading back for were the basis was during pandemic.

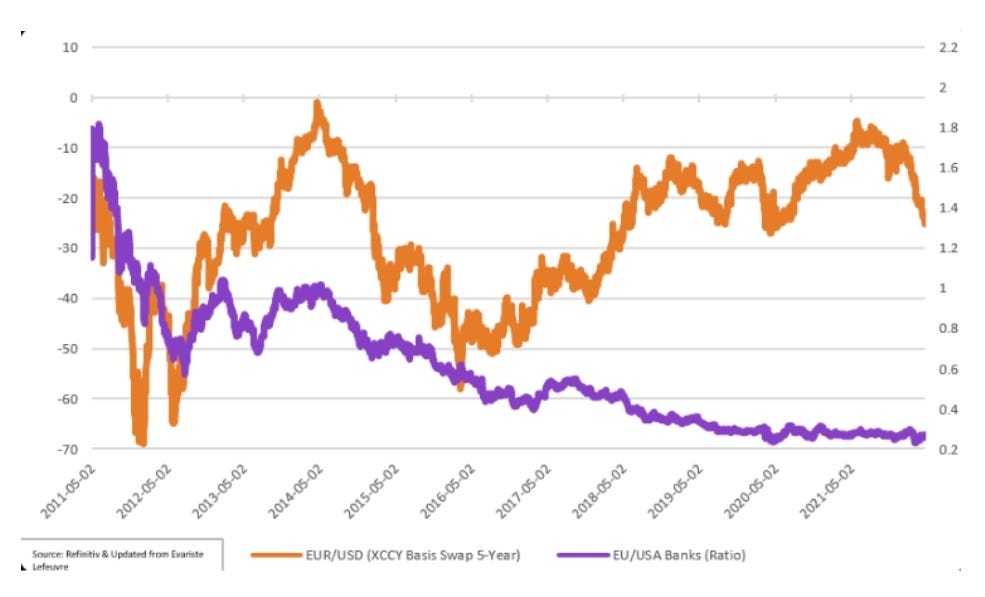

Chart 2 below that also shows that in times when you have a strong dollar the basis (which is the perceived premium) widens. Now as you can see from chart two when there is less of a strong dollar, as shown measured against the DXY the basis narrows.

In chart 2 this is the average of different currencies, and it is on the 5-year CCBS. One can see an inverse correlation between the two. Now we are starting to see a massive divergence between the two, so with this happening if that divergence continues dollar strength should continue, from simple supply and demand dynamics.

Lack of the supply (in form of dollars) high demand from institutions for need of dollars, and that pushes the basis wider (in econ101 price level up). So essentially, we are seeing a rise in the basis which you could think about as a rise in the price level to adjust for lack of supply relative to demand.

Now we have seen that there is obviously a lack of supply of dollars and high dollar demand, but cross-currency basis swaps can also measure risk.

As the BIS says, “…short-term FX swaps is much more sensitive to risk premia and bank funding strains, particularly during crisis episodes.”

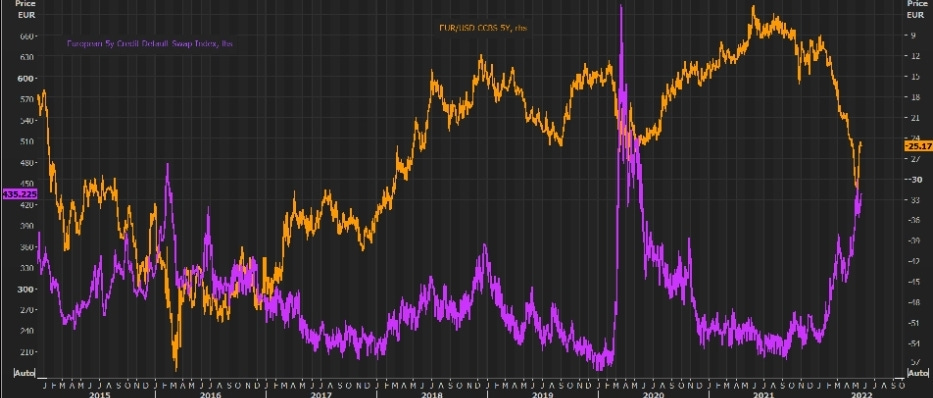

Even though these are a little bit longer in Chart 3, as was pointed out by E. Lefeuvre that as bank stocks have fallen there has been a widening in the basis swap.

This could also as the BIS has pointed out be an issue of the inability of European banks during times of crisis to access dollar funding, and when they do obviously the premium (wider basis) would be charged to incorporate increased or heighted risk.

There is also an inverse correlation between CDS for corporations on a 5-year tenor and the 5- year cross currency basis swap, as will be shown in Chart 4. This could also be unwillingness to invest in these bonds, as the increase in CDS index represents an increase to buy protection and could be to the low yields that do not want to touch these corporate bonds.

So, the correlation I believe is heighted risk and risk of default as CDS Index rises investors would rather exchange EUR for USD thus widening the basis, and again demand for dollars rises.

Finally, there is the difference in central bank ratios. Again, the credit for that chart even though I updated since the last time E. Lefeuvre published it, is the ratio between the FED’s and the ECB’s balance sheet.

What you can see as that as the Federal Reserve grows it balance sheet faster than the European Central Bank this leads to a narrow basis, and as the balance sheet of the European Central Bank grows faster than the FED it leads to a wider basis.

This is shown in Chart 5, and with the Federal Reserves current projection between the dot plot and expecting balance sheet run off this basis I am forecasting will widen even further from here.

In conclusion to all of this is a great indicator to watch. I am forecasting that the Federal Reserve will eventually be forced to back off of its tightening plan and will again drop interest rates.

The dollar funding market is already starting to see such a lack of dollars within the system, and with the treasury saying they will not be doing any new net issuance this puts further pressure on the dollar market.

With that being said the Federal Reserve, as stated should end up backing off. If they do not, I worry about the repercussions that could have across the world, and the potential for bank defaults, as many of them require USD to fund their long-term investment portfolios.

If you take that away, you start to run into the real possibility of contagion within many banking sectors.